How can you recognize some of today’s popular interior design styles? It’s probably not possible for someone to redo their entire home to fit the style, but you can always be inspired by these trends. Once you know a style you like, it’s easy to work with what you already have or buy a few accent pieces to freshen your room’s look.

Industrial This style is very popular in cities where old factories have been converted into living spaces or restaurants. It works great if you have huge windows, exposed ductwork and brick, and concrete or rustic wood flooring. Repurposing items as furniture is a big part of industrial-style. Think of using metal piping for table legs, rustic wood for table tops, old machinery parts for decorations, and repurposed industrial lighting fixtures. To make the spaces a little more comfortable, leather chairs, sheepskin floor rugs, and neutral-colored furniture are added. DIY industrial style designs

Modern To decorate in a modern style, stick with sharp edges and smooth surfaces. If your space has ceiling beams, concrete, or brick those elements should be exposed. Remove your window curtains so that natural light and the outdoor scenery shines through. Materials are natural – wood, metal, leather, wool, and linen. And, it’s important to keep the color pallet neutral colors. 20 stores that sell modern furniture

Maximalist It’s the polar opposite of minimalism. It’s been described as a rainbow of color, texture, and styles. Put your antique armchair by your new favorite sofa. Add toss pillows made from your great grandmother’s hand embroidered pillowcases. Hang your wedding photo next to a series of paintings you got on vacation. Put your collection of antique crystal decanters together on a shelf. This style is about showing off your objects and sharing the stories they tell about your life. See maximalist décor ideas

Minimalism Unlike modern design, it’s a way of life more than just a style. To be fully minimalist, you’ll need to declutter and sell or donate anything you don’t use or need. It’s uncluttered, monochromatic, and simple way of living. It works great for open floorplans, lots of light, and well built furnishings. In a minimalist room, the decorations aren’t the focus. The focus may be on a beautiful view from the window, the people in the space, or the architecture. Nothing is added as an embellishment. Steps for the beginner minimalist

Glam It’s a combo of art deco and old Hollywood. It’s opulent and a little over the top. It’s full of textures that beg to be touched – faux furs, velvet, and knits. Shiny brass and gold accents sparkle. A glam room would have classic furniture, glass or marble topped tables, crystal decorations, velvet toss pillows, rich colors, and sheer curtains. How to get a glam look in your home

Cottagecore This trend really took over while we were quarantined during Covid. It is about nostalgia, rural life, a slow pace, agriculture, with a splash of fairy-tale. It features traditional crafts like baking, gardening, knitting (all activities that became popular during quarantine). A cottagecore living room would have soft colored walls, nature-themed art, a few antique items, a hand-knit throw, potted plants, dried herbs in a basket, and a stack of books on an end table. You get extra cottagecore points if you display something you made yourself. 7 creative hobbies to take up this year

If you’re buying your first home this year, you’ll need to be extra savvy. Though competition is fierce on affordable housing, interest rates are still historically low. If you can get a home, now is a great time to do it! When you’re on the hunt for our first home, be sure to avoid these common first-time buyer mistakes:

Thinking you need 20% down payment Unless you are getting a jumbo loan, you don’t need a 20% down payment. If you chose to put down 20% for a conventional loan you won’t have to pay private mortgage insurance. But the minimum down is 3%. And other loan options may offer as little as 0% down. Of course, the more money you put down the lower your interest rate and payments will be. Talk to your home lender to see what they recommend your down payment be.

Not working with a local home lender There are a lot of home lenders out there. The reason we recommend a local lender is they have more flexibility with down payments, minimum qualifications, and the type of loan programs they can offer. As an extra bonus, they have connections in your community with realtors, inspectors, builders, and title companies. Local lenders live and work in your community, so they have more of an incentive to give you a positive experience since word-of-mouth (and not national ad campaigns) are how they get new business.

Assuming you won’t qualify Many renters don’t think they’ll be able to get a loan due to their credit or amount they have saved for a down payment. There are many different home loans, and each has its own qualifications. Some are designed for people with low credit, some offer 0% down payment, and others allow your family to gift you money for your down payment. Rather than assume you won’t qualify, make an appointment with your local home lender to see what programs they have available. They are the experts and will be able to tell you the best way for you to purchase a new home.

Underestimating repair costs Before you buy a home, hire a good home inspector to get an idea of what repairs it needs. Roofs, floors, appliances, windows… all your home’s features wear out. If you purchase an older home as a starter, you might have to pay more money to keep it in working order. The International Association of Certified Home Inspectors has a great document showing the estimated life expectancy for components in your home. If you’re working with a local lender, they’ll be able to recommend inspectors in your area.

Shopping for a house before you get pre-approved The best way to start your house hunt is by calling or visiting your loan officer. Together, you’ll set a budget for your home purchase and you’ll get an idea of what your monthly payments will be. They’ll run your credit report and pre-approve you for a home loan. In a competitive market, a pre-approval letter will let the seller know your offer is legit and will almost certainly get funded by your lender.

Not taking advantage of local first-time homebuyer programs Many states (and some communities) combine closing costs and down payment assistance programs for first time homebuyers. Some states offer tax credits you can use on your federal tax returns too. Your local lender is an expert on the current grants and programs you can take advantage of to save money.

So far in 2021, there are still less homes for sale than before Covid hit us in early 2020. But there’s an interesting trend in the homes that are being bought. More homes are being sold as secondary homes than in previous years. The National Association of Home Builders reported that 15% of all new home sales in 2020 were for second homes – that’s up from 5.5% from 2018. With housing inventory being so low, this trend is especially significant. Whether they’re buying a vacation home or investing in real estate, why might so many more homes be for secondary purposes?

Take advantage of low interest rates Even though home prices are high, interest rates are staying low. A buyer will likely overpay for your second home, but since rates are so low, you might still be in a better place financially than if you paid less but interest rates were higher. Some buyers who have had an eye on buying a secondary home may be jumping at the chance to get one with a low interest rate.

Income potential If your second home is located in an area people like to vacation, you may be in an especially good position to use it for short term rental like an Airbnb. The income from the rental may help offset the cost of HOA dues, mortgage payments, and taxes. Pay attention to how much income potential you have and compare it to the time you’ll spend cleaning the property, advertising, responding to reviews, communicating with guests, filing insurance claims for damage, and booking rentals. The average is 5 hours booking per each rental.

Alternatively, you can do long term rental for your second home. It will take less time to manage but you’ll still have to handle payments, repairs, maintenance, and communicating with your renter. You won’t have the flexibility to use the home as your own vacation spot, but you may make more income overall.

Getaway How many times have you been somewhere beautiful and dreamed of owning a little piece of that heaven? Owning a true vacation house is something a lot of people aspire to have. You just pack the car and head out for the weekend. If you maintain your home and property, you may be able to sell it for a profit some years in the future. You can even rent it out up to 14 days a year before it’s classified as an income property by the IRS.

Future retirement home Take advantage of the low interest rates and purchase your retirement home today. You can rent it out and put the income towards the mortgage payments and home upkeep. When you’re ready to retire, you can simply move in a continue to make your mortgage payments until it’s completely yours.

Long term profits Over time, the value of real estate typically increases. It’s possible to purchase a home now at low interest rates and reap the rewards over time when the home value increases. In order to be successful, you’ll need to know what your total investment in the home will be (factoring in principal, interest, maintenance, taxes, HOA dues, and more) as well as the potential for the home’s value to increase (in that past year, they’ve averaged an increase price of 9.2%).

Whatever your plans for a second home are, be sure to contact your local home lender. They’ll go over your loan options, an estimate of costs, and an estimate of your payments. With their information, you’ll be able to decide whether a second home is right for you.

People toss around terms like split-level and craftsman house styles, but what do they mean? In some regions, some styles are more popular than others. But overall, you’ve probably heard all of most of them. Let’s take a moment to go over how to identify the country’s most popular home styles, starting with the classic ranch.

Ranch

A single-story ranch home with an attached garage

It’s a long low-profile one-story home with a pitched roof, attached garage, big picture windows (often with non-functional shutters), and a sliding door leading to a patio. They were popular in the 1930’s to 1960’s and remain a popular style today. Inside is an open floor plan, vaulted ceilings, and sunken living rooms.

Mid-century modern

A mid-century modern with a double-garage and beautiful landscaping

It’s a style of home built between the 1930’s and mid 1960’s. They look contemporary and even futuristic from the outside. They showcase large windows, open spaces, sliding glass doors, geometric forms, asymmetry, minimum ornamentation, and a range of colors. Inside, they feature floor-to-ceiling windows, sunken rooms, and lots of doors to access the yard.

Contemporary

A contemporary single-family home on a large lot

This style is easily confused with modern. But, unlike modern, contemporary style is still evolving. It started in the early 2000’s. Outside, the homes are asymmetrical and irregular but with a touch of farmhouse, mid-century modern, and boho styling. The design pushes boundaries and showcase the latest technology including eco-friendly materials, smart home products, and energy efficiency. Inside, it’s all about clean lines, a minimal color pallet, and big windows to let in lots of light. They’re interior design is similar to modern, but much warmer. They have large plants, glass accent pieces, natural stone, natural fibers, and open and flexible floor plans.

Split level

Split level home with rooms above the double garage

It’s a modern style that has at least three staggered levels connected by short flights of stairs. There is a flight of stairs leading to the front door. Commonly one floor has the kitchen, living room, and dining room. A short flight of stairs goes to the upper level with bedrooms. Another short flight of stairs goes to a basement and recreational room. They often have living spaces above a connected garage. Think of the house from the Brady Bunch – that’s a split level. They became popular in the 1950’s and 1960’s.

Bi-level

Bi-level home with a bay window

When you walk up to a bi-level, the front door is level to the ground. When you open the door, there is a small landing with one short set of stairs going down to the below grade basement level and another going to the above-grade level where the kitchen and living rooms are. Since the basement is partly out of the ground, big windows bring a lot of light to the space. This style of home was popular across America the 1970’s.

Cape Cod

Cape Cod with dormer windows

Some of the first homes built in the United States were Cape Cods. They’re efficient, symmetrical, and easy to build. The front door is placed in the center of the first level and opens to the main living spaces. If there is an upper level, it’s considered a half level as it isn’t as large as the one below it – it’s essentially a converted attic space. Some homes feature dormer windows, which are individual windows (dormers) that projects out of the sloping roof to let light into the top level. They were very popular in the 1950’s and were often built with the second story left unfinished to make them even more affordable.

Colonial

A shingled colonial home

In their most basic format, American colonial homes are rectangular in shape, symmetrical, two story structures. The living room, dining room, and kitchen are located on the first level. Bedrooms are on the upper level. The front door is in the middle of the first story, and the windows all around the house are double hung with individual panes.

Dutch colonial

A Dutch colonial with shingles and gabled windows

Once you know what one is, it’s easy to pick them out. For the past 400 years, they’ve looked almost the same. They’ve got Gambrel roofs that are fairly flat on top then slope almost straight down. Sometimes they have dormer windows in the roof, but not always. People often think the roofs look like barn roofs. The design makes the attic space livable without always being considered a two-story house. Originally they were very symmetrical, but over time the style has changed and they became larger with side and rear wings.

Bungalow

A newly built bungalow with shingle accents

The name “bungalow” has its origins in India where it meant a small thatched home. We commonly use the term to define a small 1.5 story house with a low profile. They were incredibly popular around 1900 – 1930’s. Bungalows have a covered porch outside and inside feature a big living room with other rooms located around it. There are many variations on this style including California, Chicago, craftsman, arts and crafts, Milwaukee, and many more.

Victorian

A Victorian home with a large front porch

In the late 1850’s, machinery and technology advancements in America allowed builders to incorporate mass produced ornamentation for homes such as beautiful spindles, fancy brackets, and interesting shingles. The style is a tall vertical home with a mix of materials and colors. Inside, they have a grand staircase, high ceilings, many rooms, ornate wood paneling, decorative fireplaces, and hardwood floors covered with rugs.

Tudor

A Tudor-style home with brick, stucco, and half timber accents

This architecture is based on English styles from the 1600 – 1700’s. They’re easy to recognize with their steeply pitched roofs, front-facing gables (covered windows that come out of the side of the home rather than the roof), brick, and decorative half-timbers filled with stucco or stone between the spaces in the boards. They became popular in wealthy areas of Northern and Eastern parts of the United States from 1900 – 1940’s. Inside, the rooms are asymmetrical and decorated with dark wood from ceiling to floor.

Spanish eclectic

A Spanish eclectic home in the tropics

This style has its roots in the architecture of Spain and Latin America with Mediterranean accents. You’ll see them all around the United States, but they’re most popular in Florida, Texas, and California. The roofs are red or reddish-brown tile, the siding is a light-colored stucco, doors are dark wood, and you’ll often see arches over the windows, porch entries, and doors. Inside you’ll find a private courtyard, wrought-iron railings, and beautiful painted tiles along the staircases and floors.

No matter which type of home you like best, when you’re ready to buy one talk to your local Mann Mortgage lender. They’ll help you pick a budget that fits your lifestyle so you can find the perfect house to match.

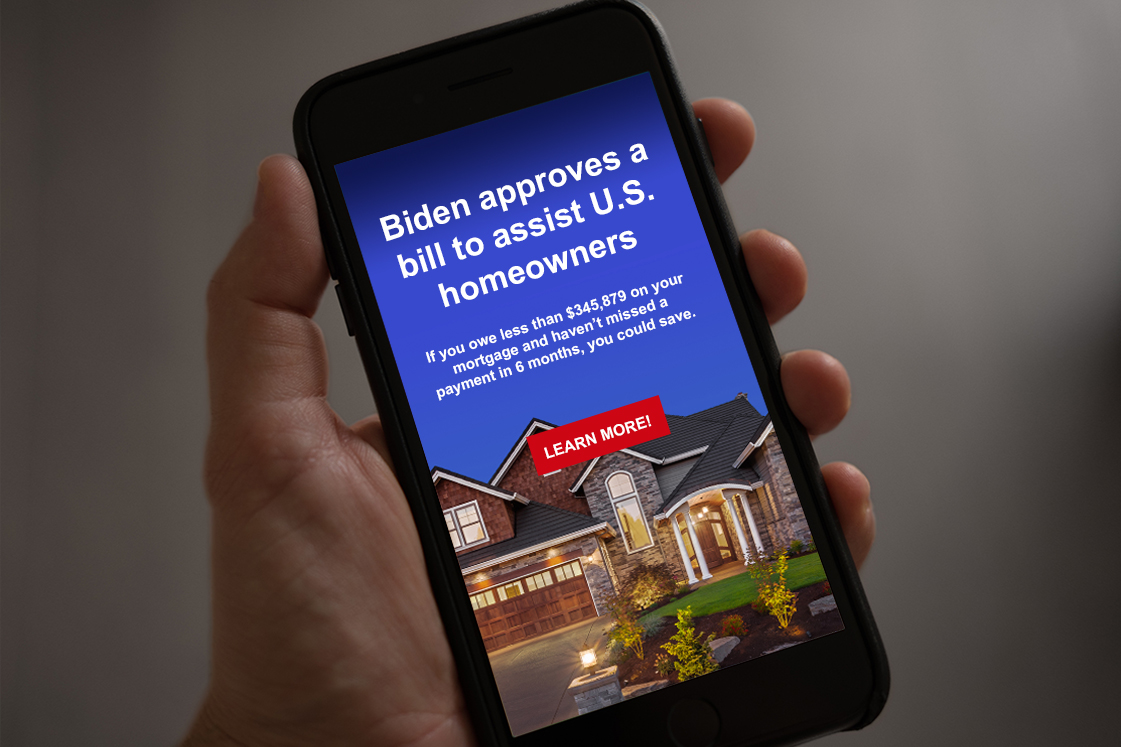

There are a lot of online ads saying some version of, “If you’re a homeowner who owes less than $300,000 on your mortgage and haven’t missed a payment in 6 months, you’re eligible for a mortgage relief program approved by Congress!”

What are these ads? Normally, if you interact with these ads you’ll be redirected to a site that will ask you your home type, credit score, loan, zip code, and more. Then they give you a list of mortgage companies to contact. Basically, these ads are great at catching your attention (they’ve been around for over a decade) then funneling you to one of the mortgage companies that has helped pay for the ad. The overall goal of these ads is for you to refinance your loan with one of the mortgage companies they are working with.

If you interact with these ads, you’ll be bombarded with more of them on YouTube, TikTok, Facebook, Google… you’ll see them everywhere. They’re harmless, but they can be annoying.

Are these programs real? Homeowners who aren’t able to make their mortgage payments do have options for help, but the claims in the ad are misleading. The mortgage amount they list and number of months of unmissed payments varies by ad and is there just to catch your attention so you click the ad.

Will the government help you pay less for your mortgage? There are government relief programs available such as the Home Affordable Unemployment Program for unemployed homeowners, Principal Reduction Alternative, the Home Affordable Foreclosure Alternatives Program, and more. Every program requires documentation and approval to use. The ad makes you feel like it’s easy to qualify, and that’s just not the case.

What can you do if you’re struggling to make your payments? Contact your home lender. Your local home lender is an expert in national, state, and community programs for assistance. In addition to assistance programs, you’ll likely hear about the two most common ways to keep your home if you are in a situation that makes it difficult for you to pay your mortgage: refinancing and forbearance.

Refinancing When interest rates are lower than you’re currently paying, it’s always a good idea to consider refinancing. A refinance means you apply to take out another mortgage to pay off and replace your original loan. If your refinance is approved, you’ll pay a fee for closing costs. In return, if your new mortgage has a lower interest rate, you may have a lower monthly payment. You could also refinance to a mortgage with a different loan term to lengthen or shorten the amount of time to pay back your loan. Or you could refinance to a different mortgage program completely. As example, homeowners with 20% equity in their home could refinance into a conventional loan to avoid paying mortgage insurance fees.

A refinance will not damage your credit and may lower your monthly payments. It can be a great option to consider.

>> Learn more about refinancing

Forbearance If you are unable to make your home payments, you can work with your lender to temporarily reduce or suspend your mortgage payments. This is called forbearance. Usually, your home lender decides whether you qualify for it and what the terms will be.

The ads you see likely play on the theme of forbearance. On occasion, Congress passes a bill to modify some terms for government-backed home loans – such as the terms for being able to go into forbearance. As an example, during the COVID pandemic, Congress put in place temporary mortgage relief under the COVID stimulus package. It’s called the CARES Act Mortgage Forbearance and applies to FHA, VA, USDA, Fannie Mae, and Freddie Mac government-backed loans (70% of homeowners have one of these loans). This bill is unique because it states your lender cannot deny your request for forbearance under the CARES Act or demand proof of financial hardship. So, it makes forbearance an option to everyone with a government-backed loan – no questions asked.

Whether you go into forbearance through government mortgage relief program or not, it will not reduce what you owe – you will have to pay back your missed payments in the future. Forbearance will appear on your credit history, but if you fulfill your part of the agreement, it won’t lower your credit score.

Can you refinance and go into forbearance at the same time? If you get a forbearance through your lender, most of them require you wait three months after forbearance ends to refinance. If you do it through a government mortgage relief program (like the CARES Act) you may be allowed to refinance while being in forbearance. Talk to your lender to see what options are available to you.

If you or a loved one are having concerns about making mortgage payments, contact your trusted home lender.

If you have a loan through Mann Mortgage, your loan officer will want to hear about your concerns, understand your current financial situation, and offer solutions to help. Don’t struggle alone. We are experts in national, state, and community programs that can help you afford your home. We’re here to make it possible for you to buy, refinance, build, and keep a home.

Deciding whether to rent or buy is complex. The right choice for you depends heavily on where you live and the local housing market. There are benefits to either option, and it’s a good idea to consider both before you make your decision.

Advantages to buying It’s a long-term investment From January 2020 to 2021, home prices nationally rose 11.2% according to the S&P CoreLogic Case-Shiller Index. Most homeowners purchase their home hoping it will be worth more money in the future. And, historically, they do appreciate in value. The amount can depend on how desirable an area it’s in, job growth in the community, housing demand, and the quality of the school district.

Easier to budget Your landlord can’t raise your rent on a whim, but they can do it when your lease ends. Give or take, it usually goes up between 3% to 5% a year. If you’re renting month-to-month, it can raise even faster – every 30 days with proper notice. With a mortgage, your rate is set when you take out your loan. If the interest rate drops, you’ll have the option to refinance and save even more. Knowing how much you’ll pay for your home for years to come is a great comfort when budgeting and planning for your future.

You can make it yours You can renovate or decorate your home to your liking. Paint the walls, redo the landscape, renovate a bathroom… your home is your canvas. And, any improvement you make could also increase your property’s value.

More privacy Compared to an apartment complex, a single-family home provides loads of privacy. You won’t hear other families, pets, music, or parties through thin walls. And, likewise, you won’t have to worry about upsetting neighbors if you decide to host a late night party.

A sense of home Buying and living in a house creates a deeper sense of permanency than renting a home. Buying or building a home is a good idea if you’d like to settle down and settle into a routine.

Advantages of renting It’s easier to relocate If you’ve got a more nomadic lifestyle, renting is perfect. You can set a countdown for once your lease is up, then you can try a new neighborhood, city, state, or country. If you rent furnished apartments, it’s even easier to pack up your things and head out to a new adventure.

Fits a transitional life If you’re lifestyle is temporary, like you are just settling into a relationship, thinking of a career move, or going to school; an apartment might suit you well. Your life may change quickly, so it’s good to have the ability to relocate or change your home size and style when you’re ready.

Worry-free maintenance Not everyone is handy or enjoys working around the house. In an apartment, you won’t have to mow the lawn, shovel the driveway, water the grass, fix a burst pipe, replace a broken appliance, or worry about any maintenance. All these activities are physical, take time, cost money, and can disrupt plans – and they can be avoided in an apartment.

Get Started in Less Than 10 Minutes

Get pre-approved with our online mortgage application. It’s simple, fast & secure!